Compare Personal Loan Rates: Financing Options Under 6%

Table of Contents

Understanding Personal Loan Interest Rates

Before diving into the hunt for low personal loan interest rates, it's crucial to grasp the basics. The Annual Percentage Rate (APR) represents the total cost of borrowing, including interest and other fees, expressed as a yearly percentage. Understanding your APR is paramount for comparing loan offers accurately.

You'll typically encounter two types of interest rates:

- Fixed Interest Rates: These remain constant throughout the loan term, offering predictability in your monthly payments.

- Variable Interest Rates: These fluctuate based on market conditions, potentially leading to varying monthly payments. While they might start lower, they can increase unexpectedly.

Several factors influence the interest rate you'll receive:

- Credit Score: Your credit history significantly impacts your eligibility for a loan and the interest rate offered. A higher credit score translates to better loan terms and lower rates.

- Loan Amount: Larger loan amounts often come with slightly higher interest rates.

- Loan Term: A shorter loan term (e.g., 12 months) typically means higher monthly payments but less interest paid overall, compared to a longer term (e.g., 60 months).

Comparing APRs from multiple lenders is essential. Online comparison tools can streamline this process, allowing you to quickly view rates from various banks and credit unions.

Finding Personal Loans with Rates Under 6%

Securing a personal loan with an interest rate under 6% requires a strategic approach. Improving your credit score is the most effective way to qualify for lower rates. This involves:

- Paying bills on time consistently.

- Maintaining low credit utilization (keeping your credit card balances low).

- Regularly checking your credit report for errors.

Beyond credit score improvement, actively shopping around and comparing offers from different financial institutions is crucial. This includes:

- Banks: Many major banks offer personal loans, but their rates can vary.

- Credit Unions: Credit unions often provide more competitive rates than banks, particularly for members.

- Online Lenders: These lenders offer convenience and may have competitive rates, but thorough research is essential.

Consider these points when comparing lenders:

- Pre-qualification: This involves a soft credit check that doesn't affect your credit score, giving you an idea of potential rates.

- Formal Application: This involves a hard credit check and a more detailed review of your financial situation.

- Negotiating: Don't hesitate to negotiate the interest rate, particularly if you have a strong credit score and multiple offers.

Secured vs. Unsecured Personal Loans: Secured loans (backed by collateral) typically offer lower interest rates than unsecured loans.

Hidden Fees and Charges to Consider

While the advertised interest rate is important, don't overlook hidden fees that can significantly increase the overall cost of your loan. Common fees include:

- Origination Fees: Charged by lenders to process your loan application.

- Prepayment Penalties: Penalties for paying off the loan early.

- Late Payment Fees: Charges for missing payments.

Always read the fine print carefully before signing any loan agreement.

Consider these points:

- Identify and avoid excessive fees: Compare the total cost of the loan, not just the interest rate.

- Calculate the total repayment amount: This includes the principal loan amount, interest, and all fees.

- Compare total costs: Use a loan amortization calculator to understand your total payments.

Alternatives to Personal Loans with Low Rates

If you're struggling to secure a personal loan with a rate under 6%, consider these alternatives:

- 0% APR Credit Cards: Some credit cards offer introductory periods with 0% APR. However, be mindful of high interest rates after the promotional period and ensure you can pay off the balance before the interest kicks in.

- Peer-to-Peer Lending: Platforms that connect borrowers with individual lenders. However, proceed with caution and thoroughly research the platform's reputation and terms.

When considering these alternatives:

- Weigh the pros and cons: Compare interest rates, fees, repayment terms, and eligibility requirements.

- Determine suitability: Consider your financial situation, credit score, and the purpose of the loan.

Conclusion

Finding a personal loan with a rate under 6% requires careful planning, research, and comparison shopping. Improving your credit score, understanding loan terms, and comparing offers from multiple lenders are crucial steps. Don't forget to factor in all fees and charges when calculating the total cost. Exploring alternative financing options can also be beneficial. Start comparing personal loan rates today! Take advantage of online comparison tools and secure the best financing options under 6% to achieve your financial goals. Remember to carefully review all terms and conditions before committing to a loan.

Featured Posts

-

Ajax Six Points Behind After Controversial Referee Decision Against Az

May 28, 2025

Ajax Six Points Behind After Controversial Referee Decision Against Az

May 28, 2025 -

Marlins At 500 After Win Against Nationals

May 28, 2025

Marlins At 500 After Win Against Nationals

May 28, 2025 -

Ou Acheter Le Samsung Galaxy S25 Ultra 1 To Au Meilleur Prix

May 28, 2025

Ou Acheter Le Samsung Galaxy S25 Ultra 1 To Au Meilleur Prix

May 28, 2025 -

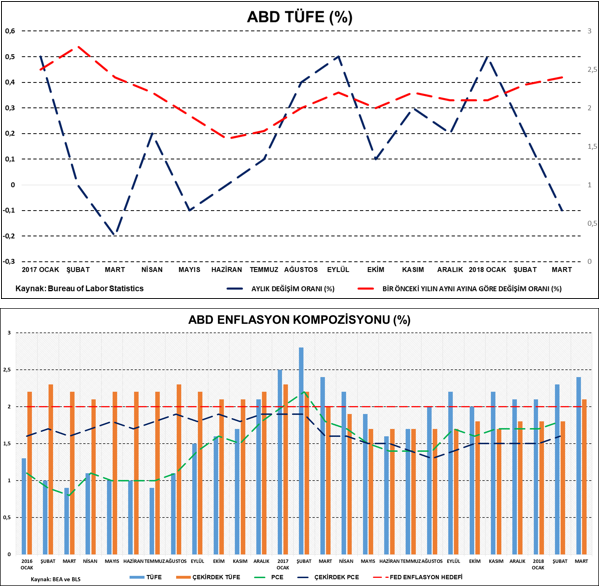

Abd Tueketici Kredileri Mart Ayi Verileri Ve Ekonomik Etkileri

May 28, 2025

Abd Tueketici Kredileri Mart Ayi Verileri Ve Ekonomik Etkileri

May 28, 2025 -

Jennifer Lopezs Next Gig Hosting The 2025 Amas

May 28, 2025

Jennifer Lopezs Next Gig Hosting The 2025 Amas

May 28, 2025

Latest Posts

-

Alcaraz Claims Monte Carlo Masters Title Despite Tough Competition

May 30, 2025

Alcaraz Claims Monte Carlo Masters Title Despite Tough Competition

May 30, 2025 -

Alcaraz Wins First Monte Carlo Masters Title After Challenging Week

May 30, 2025

Alcaraz Wins First Monte Carlo Masters Title After Challenging Week

May 30, 2025 -

330 000 Marketing Contract Via Rails Shift To High Speed Rail In Quebec

May 30, 2025

330 000 Marketing Contract Via Rails Shift To High Speed Rail In Quebec

May 30, 2025 -

Definitys Strategic Acquisition Of Travelers Canadian Operations

May 30, 2025

Definitys Strategic Acquisition Of Travelers Canadian Operations

May 30, 2025 -

Tech Companies And Mass Violence The Problem Of Algorithmic Radicalization

May 30, 2025

Tech Companies And Mass Violence The Problem Of Algorithmic Radicalization

May 30, 2025