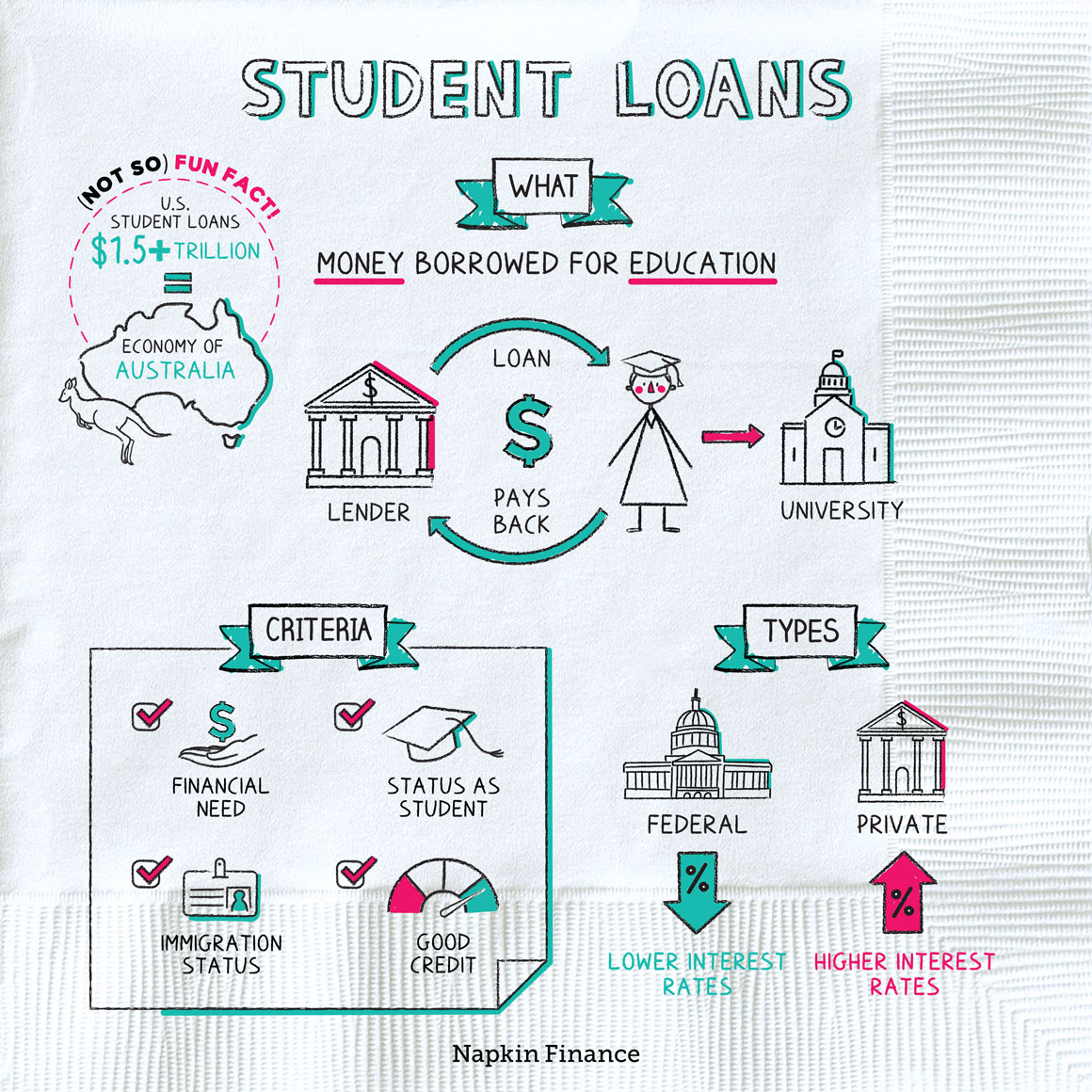

Federal Student Loan Refinancing: Should You Use A Private Lender?

Table of Contents

Understanding Your Federal Student Loan Options

Before considering private refinancing, it's crucial to understand the strengths and weaknesses of your existing federal student loans.

Benefits of Federal Student Loans

Federal student loans offer significant advantages that you might lose upon refinancing with a private lender. These include:

- Income-driven repayment plans: These plans adjust your monthly payments based on your income and family size, making repayment more manageable during periods of financial hardship. Keywords: income-driven repayment, student loan repayment plans.

- Forgiveness programs: Programs like Public Service Loan Forgiveness (PSLF) and Teacher Loan Forgiveness can eliminate a portion or all of your remaining debt after meeting specific criteria. Keywords: federal loan forgiveness, student loan forgiveness programs.

- Deferment and forbearance options: Federal loans allow for temporary pauses in payments under certain circumstances, such as unemployment or financial hardship. Keywords: student loan deferment, student loan forbearance.

Disadvantages of Refinancing Federal Loans

Refinancing federal student loans with a private lender means giving up the valuable protections offered by the federal government. This can have serious consequences:

-

Loss of federal loan forgiveness programs: Refinancing eliminates your eligibility for programs like PSLF and Teacher Loan Forgiveness.

-

Loss of flexible repayment options: You'll lose access to income-driven repayment plans, potentially leading to higher monthly payments.

-

Increased risk during financial hardship: Without deferment or forbearance options, you could face default if you experience unexpected job loss or illness.

-

Specific federal programs that could be lost:

- Public Service Loan Forgiveness (PSLF)

- Teacher Loan Forgiveness

- Income-Driven Repayment (IDR) plans (IBR, PAYE, REPAYE)

The Allure of Private Student Loan Refinancing

While losing federal protections is a significant drawback, private student loan refinancing offers its own appeal.

Potential Benefits of Private Refinancing

Private lenders may offer:

- Lower interest rates: If you have a good credit score, you may qualify for a lower interest rate than your current federal loan rate, potentially saving you money over the life of the loan. Keywords: lower interest rates, student loan interest rates.

- Simplified repayment: Consolidating multiple federal loans into a single private loan simplifies your repayment process. Keywords: student loan repayment, loan consolidation.

- Shorter repayment term: A shorter repayment term means you'll pay off your debt faster, but with potentially higher monthly payments.

Factors Affecting Private Refinancing Rates

Several factors determine the interest rate you'll receive from a private lender:

-

Credit score: A higher credit score generally qualifies you for a lower interest rate. Keywords: credit score, interest rate, student loan debt.

-

Income: Lenders consider your income to assess your ability to repay the loan.

-

Loan amount: The amount you borrow also affects your interest rate.

-

Factors to consider before choosing a private lender:

- Your credit score

- Your income and debt-to-income ratio

- Your employment stability

- The interest rate offered

- The repayment terms

- The fees associated with the loan

Comparing Federal and Private Refinancing Options

To make an informed decision, compare the key features of both options.

A Side-by-Side Comparison

| Feature | Federal Refinancing | Private Refinancing |

|---|---|---|

| Interest Rates | Generally higher | Potentially lower (depending on credit score) |

| Fees | Typically lower or nonexistent | May include origination fees and other charges |

| Repayment Terms | Flexible options available | Typically fixed, potentially shorter |

| Government Benefits | Income-driven repayment, forgiveness programs | None |

Considering Your Financial Situation

Your individual financial circumstances heavily influence the best choice.

-

Credit score: A high credit score significantly improves your chances of getting a favorable rate with a private lender.

-

Debt-to-income ratio: A high debt-to-income ratio might make it difficult to qualify for private refinancing.

-

Employment stability: Lenders prefer borrowers with stable employment.

-

Importance of comparing multiple lenders: Shop around and compare offers from different private lenders to find the best terms.

-

Carefully review loan terms and conditions: Don't rush into a decision; thoroughly examine all aspects of the loan agreement.

Choosing the Right Private Lender (if applicable)

If you decide to pursue private refinancing, choosing the right lender is crucial.

Factors to Consider When Selecting a Private Lender

- Interest rates: Compare rates from multiple lenders. Keywords: best student loan refinance lenders, low interest student loans.

- Fees: Be aware of any origination fees, prepayment penalties, or other charges. Keywords: loan fees, student loan refinance fees.

- Customer service: Read reviews to assess the lender's responsiveness and helpfulness. Keywords: customer reviews, student loan lender reviews.

- Lender reputation: Choose a reputable and established lender. Keywords: reputation, student loan refinance lenders.

Due Diligence Before Refinancing

Thorough research is essential.

- Reputable sources for researching lenders: Check websites like the Consumer Financial Protection Bureau (CFPB) and the Better Business Bureau (BBB).

- Risks associated with unreliable lenders: Be wary of lenders with hidden fees, predatory practices, or poor customer reviews.

Conclusion: Making Informed Decisions About Federal Student Loan Refinancing

Refinancing federal student loans with a private lender offers the potential for lower interest rates and simplified repayment, but it comes at the cost of valuable federal protections like forgiveness programs and flexible repayment options. Carefully weigh the pros and cons, considering your credit score, debt-to-income ratio, employment stability, and long-term financial goals. Compare offers from multiple lenders, meticulously read the fine print, and prioritize choosing a reputable institution. Carefully weigh the pros and cons of federal student loan refinancing before choosing a private lender. Make an informed decision to best manage your student loan debt. Consider your options for private student loan refinance carefully to find the best solution for your unique circumstances.

Featured Posts

-

Seattle Mariners Vs Detroit Tigers Injury Report For Series March 31 April 2

May 17, 2025

Seattle Mariners Vs Detroit Tigers Injury Report For Series March 31 April 2

May 17, 2025 -

Rockwell Automation Beats Expectations Joining Other Winning Stocks

May 17, 2025

Rockwell Automation Beats Expectations Joining Other Winning Stocks

May 17, 2025 -

Jack Bit The Top Bitcoin Casino In The Usa

May 17, 2025

Jack Bit The Top Bitcoin Casino In The Usa

May 17, 2025 -

Refinancing Federal Student Loans With A Private Lender What You Need To Know

May 17, 2025

Refinancing Federal Student Loans With A Private Lender What You Need To Know

May 17, 2025 -

Secret Service Investigation Into White House Cocaine Incident Ends

May 17, 2025

Secret Service Investigation Into White House Cocaine Incident Ends

May 17, 2025

Latest Posts

-

Uber Mumbai Pet Travel Policy And Booking Guide

May 17, 2025

Uber Mumbai Pet Travel Policy And Booking Guide

May 17, 2025 -

Top Australian Crypto Casino Sites For 2025

May 17, 2025

Top Australian Crypto Casino Sites For 2025

May 17, 2025 -

Mirax Casino A Top Rated Ontario Online Casino For 2025

May 17, 2025

Mirax Casino A Top Rated Ontario Online Casino For 2025

May 17, 2025 -

Best Bitcoin And Crypto Casinos In 2025 The Ultimate Guide

May 17, 2025

Best Bitcoin And Crypto Casinos In 2025 The Ultimate Guide

May 17, 2025 -

Best Online Casinos Ontario Mirax Casino Top Payouts In 2025

May 17, 2025

Best Online Casinos Ontario Mirax Casino Top Payouts In 2025

May 17, 2025