Privatizing Student Loans: Examining Trump's Potential Approach

Table of Contents

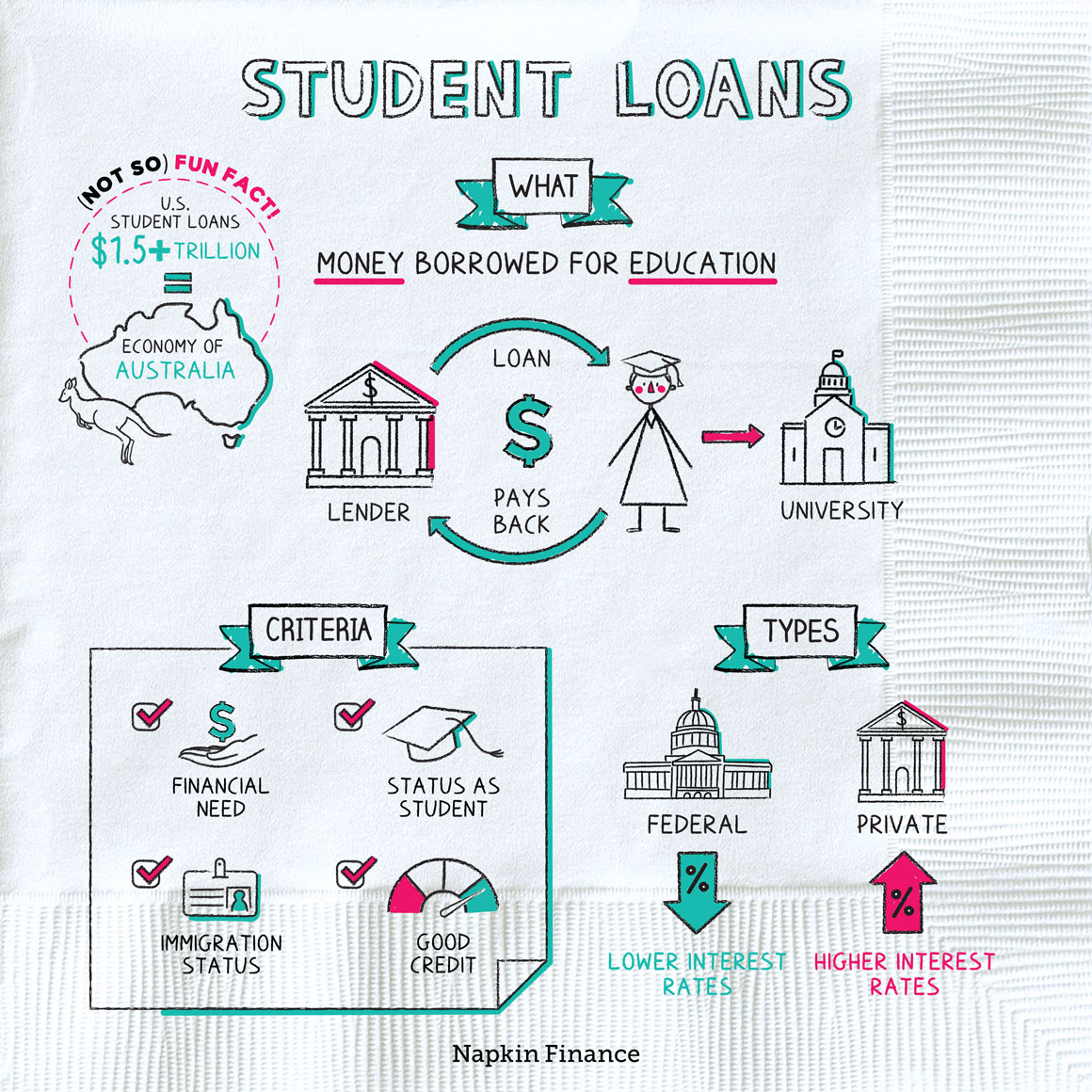

The Trump Administration's Stance on Student Loan Debt

Campaign Promises and Statements

During his presidential campaigns, Donald Trump made several statements regarding student loan debt, though a comprehensive plan for privatization wasn't explicitly detailed. His rhetoric often focused on reducing the burden of student debt, but the methods proposed were varied and sometimes contradictory.

- Quote 1 (Example): "We need to make it easier for students to pay off their loans..." (Insert actual quote here if available). This statement, while supportive of debt relief, doesn't directly address privatization.

- Quote 2 (Example): "...we will explore ways to reduce the cost of higher education..." (Insert actual quote here if available). This hints at addressing the root causes of debt but doesn't specifically advocate for privatizing the loan system.

- Potential Policy Shifts: A Trump-like approach might involve shifting the responsibility of loan disbursement and management from the federal government to private entities, potentially impacting interest rates, repayment terms, and accessibility to education loans.

Existing Government Programs and Their Potential Privatization

The current federal student loan system comprises several key programs:

- Direct Loan Program: This program, administered directly by the federal government, offers subsidized and unsubsidized loans to eligible students. Privatization could mean transferring this administration to private lenders.

- Federal Family Education Loan (FFEL) Program: While largely phased out, understanding its history is crucial. Its privatization – and the subsequent issues – offers valuable lessons.

- Pros and Cons of Privatization: While privatization could potentially reduce the federal budget deficit by removing the government's role in loan guarantee, it also carries risks. Private lenders may prioritize profit over accessibility, potentially leading to higher interest rates and stricter lending criteria, potentially excluding low-income students.

Potential Models for Privatizing Student Loans

Different Privatization Models

Several models exist for privatizing the student loan system:

- Complete Transfer to Private Lenders: This would involve completely handing over the responsibility of student loans to private banks and financial institutions. This model carries significant risks, as it could lead to predatory lending practices and increased inequality in access to higher education.

- Government-Backed Private Loans: The government would continue to guarantee loans provided by private lenders, mitigating some of the risks but still leading to potential issues with interest rate fluctuations and access.

- Voucher Systems: Students would receive government vouchers to use towards tuition at approved institutions, but the loans themselves would be handled by private entities. This model offers more control but can be complex to administer.

Comparisons: A complete transfer model offers the most significant reduction in government involvement, but also carries the greatest risk. A voucher system offers a balance, but necessitates stringent regulations to prevent abuse. Government-backed loans offer a degree of protection but still expose students to market fluctuations.

Role of Private Lenders

Private lenders would play a central role in any privatization model. Their incentives are profit-driven, leading to potential conflicts of interest.

- Potential Benefits for Private Lenders: Increased profitability through higher interest rates, fees, and larger loan volumes.

- Potential Risks for Private Lenders: The risk of loan defaults increases if the government's safety net is removed or weakened.

- Implications for Borrowers: Increased interest rates, stricter lending criteria, and potentially less favorable repayment terms could burden borrowers, particularly those from disadvantaged socioeconomic backgrounds.

Economic and Social Implications of Privatizing Student Loans

Impact on Student Borrowers

Privatization would significantly affect students:

- Increased Interest Rates: Private lenders are likely to charge higher interest rates compared to government-subsidized loans.

- Changes in Loan Terms: Repayment plans could become less flexible, increasing the burden on borrowers.

- Increased Defaults: Higher interest rates and stricter terms could lead to a higher default rate, further impacting borrowers' credit scores and financial well-being.

- Disadvantage for low-income students: Access to higher education could become increasingly restricted for students from low-income backgrounds who may not qualify for private loans.

Effects on the Higher Education Market

The higher education landscape would also transform:

- Tuition Fees: Universities might raise tuition fees in anticipation of increased loan availability from private lenders.

- Enrollment Patterns: Increased cost could deter some students from pursuing higher education.

- Accessibility: The accessibility of higher education would likely decrease, particularly for students from underprivileged backgrounds.

Long-Term Economic Consequences

Privatizing student loans has profound macroeconomic implications:

- Reduced Government Spending: The government could save money by offloading loan administration, but this benefit might be offset by increased social costs.

- Increased Inequality: Privatization could exacerbate existing socioeconomic inequalities in access to higher education.

- Financial Instability: A sudden increase in loan defaults could create instability in the financial system.

- Market Failures and Regulatory Challenges: The market might not effectively regulate itself, necessitating significant government oversight and potential regulations to prevent exploitation of students.

Conclusion: Privatizing Student Loans: A Critical Assessment of Trump's Potential Approach

Privatizing student loans under a Trump-like approach presents a complex dilemma. While it could potentially reduce government spending, the potential drawbacks, including increased costs for students, reduced access to higher education, and increased financial risk for both students and the overall economy, are significant. The benefits of reduced government involvement must be carefully weighed against the potential negative social and economic consequences. A balanced approach that considers the needs of students from diverse socioeconomic backgrounds is essential.

To make informed decisions about the future of student loan financing in the US, it's vital to continue researching the complexities of "privatizing student loans" and engaging in open and informed discussions about its potential consequences. For more information, explore resources from the Department of Education, consumer finance protection agencies, and independent research organizations focusing on higher education finance. Understanding the various models and their implications is crucial to shaping a future where higher education is accessible and affordable for all.

Featured Posts

-

Josh Cavallo Leading The Way For Lgbtq Inclusion In Sport

May 17, 2025

Josh Cavallo Leading The Way For Lgbtq Inclusion In Sport

May 17, 2025 -

Section 230 And Banned Chemicals A Recent Legal Decision Affecting E Bay

May 17, 2025

Section 230 And Banned Chemicals A Recent Legal Decision Affecting E Bay

May 17, 2025 -

Refinancing Federal Student Loans With A Private Lender What You Need To Know

May 17, 2025

Refinancing Federal Student Loans With A Private Lender What You Need To Know

May 17, 2025 -

Nestle And Shell Rebuff Musks Boycott Claims Advertisers Respond

May 17, 2025

Nestle And Shell Rebuff Musks Boycott Claims Advertisers Respond

May 17, 2025 -

La Landlord Price Gouging A Real Estate Agents Perspective On The Fire Aftermath

May 17, 2025

La Landlord Price Gouging A Real Estate Agents Perspective On The Fire Aftermath

May 17, 2025

Latest Posts

-

Top Rated Online Casinos In New Zealand 7 Bit Casino And Alternatives

May 17, 2025

Top Rated Online Casinos In New Zealand 7 Bit Casino And Alternatives

May 17, 2025 -

Best Online Casinos In New Zealand 7 Bit Casino Review And Top Picks

May 17, 2025

Best Online Casinos In New Zealand 7 Bit Casino Review And Top Picks

May 17, 2025 -

Investing In The Future Of Uber Driverless Car Etfs And Their Potential

May 17, 2025

Investing In The Future Of Uber Driverless Car Etfs And Their Potential

May 17, 2025 -

Ubers Autonomous Vehicle Future Investing In Driverless Tech Etfs

May 17, 2025

Ubers Autonomous Vehicle Future Investing In Driverless Tech Etfs

May 17, 2025 -

Could Driverless Uber Pay Off Etf Investing In Autonomous Vehicle Technology

May 17, 2025

Could Driverless Uber Pay Off Etf Investing In Autonomous Vehicle Technology

May 17, 2025